Passage of largest American banks through the market shock generated by coronavirus: exposure to ESG score

The study analyses the relationship between ESG scores and shock parameters, finding that high ESG banks perform better on these parameters. The study also examines changes in the ESG scores of the top 50 US banks from 2018 to 2022. Furthermore, the study clusters banks based on various indicators, including total assets, SD, RR, and K ratio. The study concludes that ESG criteria are relevant in times of crisis. ESG scores are important indicators of banks that extend the traditional riskreturn correspondence.

The pandemic generated by the coronavirus has had a different impact on the global economy. One of the components was the shock that hit financial markets. It was characterized by a sharp fall in stock prices and a relatively rapid recovery. Today, much attention is paid to the study of this shock. Different approaches are used. As an example, the approach “event study” is applied intensively (ex. [1]). Another approach focuses on to shape of the curve which characterizes stock pricing passage of shock. Typically, researchers distinguish L, V, U, and W types of shapes [2].

In our research, the goal is to find out how the ESG level (Environmental, Social, Governance) in banks influenced the shock passage and vice versa, how the shock parameters affected that level. A similar study was conducted for the 50 largest (by assets) banks in the US. It should be noted that today in the segment of financial investments, the consideration of ESG criteria has become an important component of investment decision-making. In this case, the level of implementation of ESG criteria in its activities in numerical form is estimated by ESG scoring. This score is calculated by a number of companies, including Standard & Poors, Refinitiv, Sustainalytics and other. We chose to study ESG scoring of Standard & Poors. Because they include, among other things, a representation of the dynamics of ESG scorings values.

In the first part of our study we used an analysis of the relationship between ESG score and a pair of indicators (SD; RR):

Shock Deepness = (minimum price at shock period) / (average price at before shock period) - 1

Recovery Rate = (Average price at after shock period) / (Average price at before shock period)

Our investigation showed that banks with high ESG scoring scores showed better values of this pair: their stocks fell less, and they recovered better.

| ESG scoring (2018) | SD | RR |

|---|---|---|

| Higher than 60 | -24,9% | 78,8% |

| 30-59 | -29,3% | 71,9% |

| Lower than 30 | -30,3% | 73,8% |

In the second part of the study, we analyzed how ESG score of banks in 2022 has changed in comparison with values in 2018. An interesting result is the dependence of changes on both assets and the ratio of deposits to assets.

| ∆ESG | 0,2-0,6 | 0,6-0,8 | 0,8-0,85 | 0,85+ |

|---|---|---|---|---|

| >1000 | -6 | -5,3 | х | х |

| 300-1000 | х | 1,64 | х | х |

| 100-300 | 0,75 | 0,875 | 6,1 | 3,5 |

| <100 | 0,5 | х | 4,3 | 2,35 |

As you can see, the largest amount of ESG scores lost banks with assets over a trillion dollars. And the improvement in scoring scores was shown by small banks with a deposit-to-asset ratio of more than 80%. We estimate that during the shock, this group was improving on S and G.

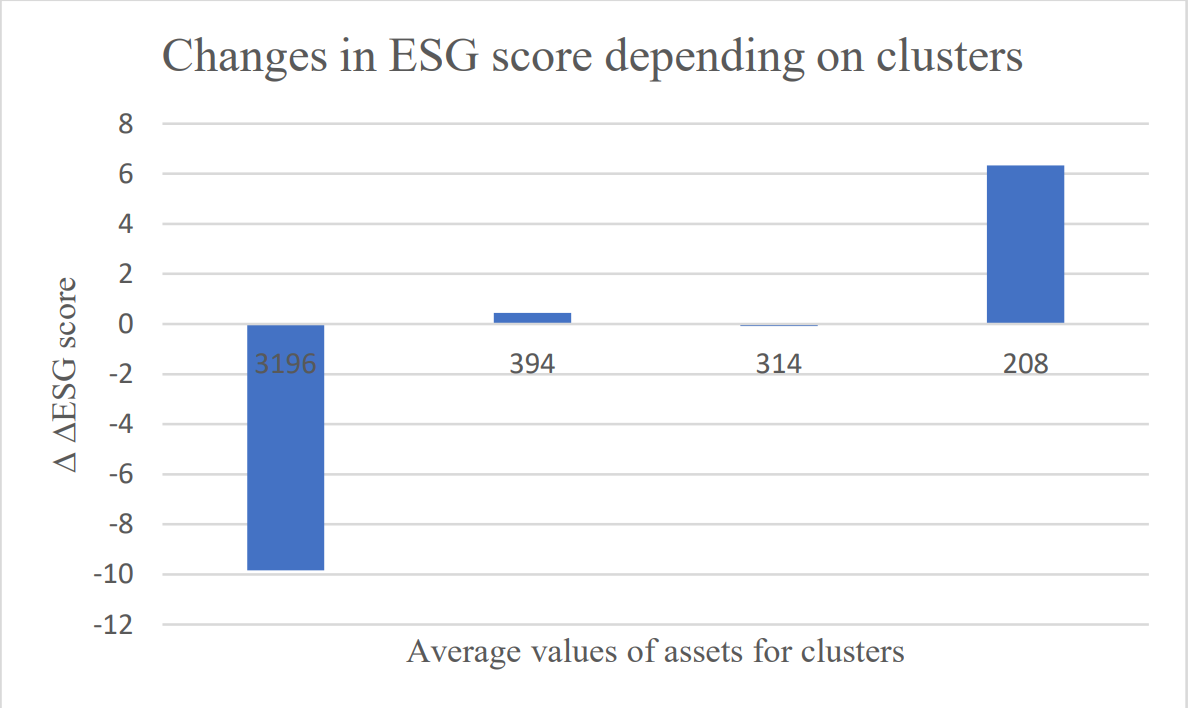

In the next step, we conducted a more in-depth study. It included the application of bank clustering based on 4 indicators: Total Assets, SD, RR, K-ratio [4]. The result includes identification 4 clusters. The dependences between ESG scores changes and average total assets at clusters present in the graph.

At the same time, the changes of K-ratio, which we consider to be the market indicator consistency, showed the greatest increase for banks that have values of assets 300-400 Bln USD.

Overall, the study shows that ESG criteria are relevant when considering transition through crisis. They affected the depth of the fall in banks’ stocks during the coronavirus shock. At the same time, the crisis itself affected them. Thus, ESG score is an important indicator of banks, which expands the classic risk-return correspondance

References

- Khatatbeh, Ibrahim & Bani Hani, Mohammad & Alfoul, Mohammed. (2020). The Impact of COVID-19 Pandemic on Global Stock Markets: An Event Study. International Journal of Economics and Business Administration. VIII. 505-514.

- Mahata, Ajit & Rai, Anish & Nurujjaman, Md. & Prakash, Om, 2021. “Modeling and analysis of the effect of COVID-19 on the stock price: V and L-shape recovery,” Physica A: Statistical Mechanics and its Applications, Elsevier, vol. 574(C).

- Kaminskyi Andrii , Nehrey Maryna. Changing Risk-Return Correspondence during the COVID-19 Turmoil : Evidence from Polish Stock Market. Research on Enterprise in Modern Economy - theory and practice (REME), 2021, vol. 1, nr 32, s. 18-33

- Kestner, Lars N., (Re)Introducing the K-Ratio (March 3, 2013). Available at SSRN: https://ssrn.com/abstract=2230949 or http://dx.doi.org/10.2139/ssrn.2230949